Passenger cars

Putting hybrid fluids to the test

21 April 2026

21 April 2026

Car makers call for simplification and flexibility to ensure Europe remains a viable marketplace

The European automotive industry is going through a tough time. Rising global competition, fragile supply chains and inflexible decarbonisation mandates have prompted calls from OEMs for a stronger Automotive Package to ensure Europe remains a viable marketplace for cars and vans beyond 2030. Against this backdrop, Insight examines the region’s latest vehicle sales trends and the challenges automakers are facing and explores what the industry says it needs to better align climate ambitions with business growth.

First, to set the scene, let’s look at passenger car sales trends in the ‘European market’ - comprising the European Union, the EFTA states (Iceland, Norway, and Switzerland), and the United Kingdom. According to data from the European Automobile Manufacturers’ Association (ACEA), sales were up 2.4% in 2025 vs 2024, reaching just over 13.2 million. Looking at sales by powertrain for 2025, full battery electric vehicle (BEV) sales grew to reach almost 2.6 million, and sales of hybrids exceeded 5.8 million, while sales of conventional petrol and diesel cars fell.

However, sales volumes in wider Europe remain well below the pre-pandemic levels of more than 15 million units. Comparing the powertrain split to that of 2018, it is clear that conventional diesel and petrol powered vehicles are losing market share. While electrified vehicle sales have grown to account for two thirds of sales in the region, full BEV represent just under 20% of total sales, with most growth seen for hybrid electric vehicles (HEV).

The sales data highlight the first challenge for European automakers – volumes are down. Customers, although shopping with more of an environmental conscious, are also price sensitive, which in part accounts for the slow uptake of BEV vs HEV.

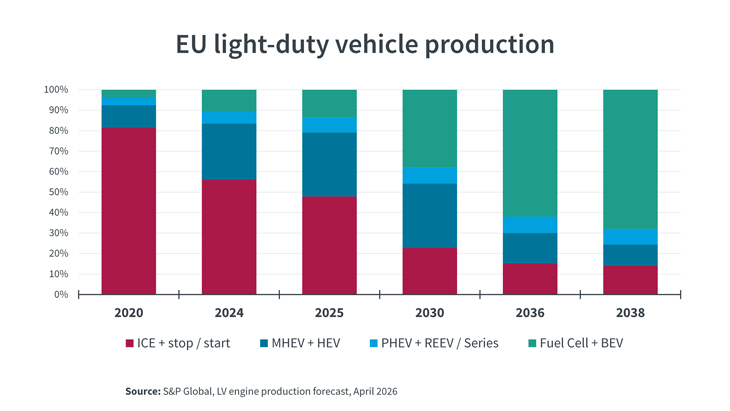

Looking ahead at projected European production, market analysts S&P Global forecasts continued hybrid growth out to 2030. However, the picture of BEV dominance post 2035 could change significantly if the European Commission (EC) continues to soften its approach regarding future technology options. In addition, the forecast data show production volumes only increasing by half a million in 2030 vs 2035 – suggesting continued slow sales. Again, with increasing geo-political tension, high oil prices and continued economic uncertainty, these figures could be subject to further change.

The relatively low BEV uptake presents a second challenge for European OEMs in terms of reaching net zero emissions. In 2025, some 80% of vehicles sold contained an internal combustion engine (ICE). In hybrids, depending on the configuration, the ICE can be used to drive the wheels or as an onboard generator to produce electricity for the battery or electric motor. These models are popular with consumers owing to their lower purchase price vs BEV and lack of range anxiety.

However, until recently, the EC had intended to ban the sale of ICE-powered light-duty vehicles by 2035 – an action that has been pushing OEMs down a BEV-only technology path for customers in Europe. This presents a number of challenges to OEMs who are trying to support the energy transition while also creating a healthy European automotive industry and providing affordable mobility for everyone.

In its latest Economic and Market Report ACEA says that in 2025 the European car sector faced significant headwinds. In value terms, imports fell by 3.2% and exports by 6.2%, which added further pressure to the trade surplus, which now stands at €76 billion. The imbalance with China was particularly stark as EU exports contracted by 4.3% whilst imports from China continued to rise – surpassing 1 million units for the first time, which represents over a quarter of total EU car imports from third countries. ACEA says these trends point to a weakening of external demand for EU-made vehicles.

The economic health of the EU car industry is relatively poor, and a number of European OEMs are currently reporting significant profit pressure.

One challenge comes from Chinese OEMs, who are facing increasing saturation in their domestic market and a gradual reduction in policy‑driven incentives. These pressures are pushing them to rely more heavily on overseas growth and we are already seeing plans from major automakers, such as BYD and Chery, to ‘go local’ in Europe, which could further impact sales for European OEMs. Looking at vehicle sales data from ACEA, Chinese brands grew to reach more than 49,000 units in 2025, 3.7% of total European market sales. Most significantly, BYD sales were up more than 227% in 2025 vs 2024. The most recent data suggest this trend is continuing, with sales of Chinese brands in January and February 2026 capturing almost 4% of all new vehicle sales in Europe.

In December 2025, the EC took action that it says is designed to support a clean and competitive automotive sector, which included a slight softening on the planned ICE ban.

“We want our industries to be the leaders of the transition to a low-carbon economy because that is what is best for our climate, competitiveness and independence.”

Wopke Hoekstra, Commissioner for Climate, Net Zero and Clean Growth

The Automotive Package recognised the need for more flexibility and technology neutrality to make the green transition a success, and it introduced major changes compared to the current law.

According to the Commission, the package sets an ambitious yet pragmatic policy framework to ensure 2050 climate neutrality and strategic independence, while providing more flexibility to manufacturers. It also responds to calls by the EU industry to simplify rules.

Key changes, designed to addresses both supply and demand of the automotive sector's transition include:

Review of existing CO2 emission standards for cars and vans.

Flexibility to support the industry and enhance technological neutrality.

Super Credits for small affordable electric cars made in the European Union.

Battery Booster to accelerate the development of a fully EU-made battery value chain.

Automotive Omnibus to ease administrative burden and cut costs for European manufacturers.

Mandatory targets to support the uptake of zero- and low-emission vehicles by large companies in their corporate vehicles.

“We are strengthening the sector’s competitiveness introducing flexibility into the CO₂ standards for cars and vans and a technology neutral framework.”

Apostolos Tzitzikostas, Commissioner for Sustainable Transport and Tourism

Looking specifically at the changes in CO2 emissions standards. What the EC has proposed from 2035 onwards, is that carmakers must comply with a 90% tailpipe emissions reduction target from 2021 levels. The remaining 10% of emissions will need to be compensated through the use of low-carbon steel made in the Union, or from e-fuels and biofuels. The EC says this change means plug-in hybrids, range extenders, mild hybrids, and internal combustion engine vehicles will continue to play a role in new car sales beyond 2035, in addition to full electric and hydrogen vehicles.

While these measures were well received by OEMs, they did not do enough, in their opinion, to address the issues the industry is currently facing, while other industry bodies were concerned about the risks of backtracking on the 2035 zero-emission target.

ACEA, which represents the 17 major Europe-based automobile manufacturers, including the three largest Volkswagen Group, Stellantis and Renault Group, clearly has reservations about the support the changes will deliver. In a statement the organisation said, the Automotive Package is a first step to creating a more pragmatic and flexible pathway to align decarbonisation with competitiveness and resilience objectives, but it needs more decisive measures to facilitate the transition in the next few years.

“Attaching strict conditionalities to various elements of the package may have a counterproductive effect on technology openness and competitiveness.”

ACEA

Stellantis, although an ACEA member said separately that the introduction of technology neutrality through the revision of the 2035 CO2 reduction target is an important step but, as currently proposed, it will not support the production of affordable vehicles for the vast majority of customers.

The International Council on Clean Transportation (ICCT), an organisation providing technical and scientific analysis to environmental regulators, says that under the proposed revised regulation, total projected car CO2 emissions would rise by more than 18% from 2028–2050 vs the previous regulation. It says it is essential that the proposed mechanisms to offset the additional CO2 emissions and to accelerate the uptake of small affordable electric vehicles are robust and unambiguous. By addressing the gaps and questions in the current proposal, ICCT says the EU can keep its climate ambitions on track while supporting affordable electric mobility.

“Stumble on the details and the proposal could pave the

way for excess emissions and forfeited leadership in the global race to zero.”

The International Council on Clean Transportation

Since the EC announcement, stakeholders have been busy studying the package and working with co-legislators to critically strengthen the proposals where needed.

In March, ACEA set out conditions for a stronger EU Automotive Package that it sees as critical if Europe is to maintain its global automotive leadership.

While ACEA agrees that decarbonisation is the way forward, it says the flexibility proposed in the package is insufficient to transform the automotive industry in the real world. Without a tripling of the EU BEV market in four years, ACEA fears EU manufacturers face the risk of crippling fines. Currently the new EC proposal includes an averaging of the 2030 target, which means carmakers will be allowed to average their emissions over three years, rather than achieve their objectives in 2030. ACEA suggests the proposed three year averaging window for compliance is extended to five years (2028-2032) and the list of flexibilities and compensatory mechanisms for compliance beyond small and ‘made in the EU’ BEV are also extended.

ACEA also says that despite the proposed compensation mechanisms, credits for low-carbon steel, and sustainable renewable fuels, the EC’s 2035 proposal still sets 100% emissions reduction as the compliance threshold for avoiding penalties. In their view, this is not workable, and they suggest the threshold is lowered to 90% and the compensation mechanisms, which constitute an essential flexibility, should become more feasible.

“The current targets remain highly ambitious and can only be met alongside consistent EU-wide measures that genuinely boost demand.”

ACEA

However, clean transport and energy advocates, Transport and Environment (T&E), says weakening the 2035 zero-emission target to a 90% reduction target and reversing the EU’s 2035 phase-out of combustion engine sales sends a confusing signal at a time when European manufacturers urgently need to catch up with Chinese EV-makers.

In addition, T&E says the proposed three year averaging delays the EV transition and their analysis estimates BEV sales would fall to 47% in 2030 instead of reaching 57% under the current regulation. In their view, limiting the averaging to two years (2030-2031) or adding a 5% borrowing cap, BEV sales would represent around 50% in 2030, ensuring the sufficient BEV momentum and mass market adoption. The organisation says allowing five years averaging would limit BEV sales to 39%.

Despite the distraction of this activity regarding future regulations, the industry still needs to sell cars. After a shaky January, by the end of February 2026 year to date ACEA reports that new car sales were down in the wider European market by just 1%. Battery electric cars accounted for almost 20% of the market share in January-February 2026, while hybrid-electric car registrations captured over 48% of the market over the same period, remaining the preferred choice for consumers across the region.

We will watch with interest to see how the market evolves and how the actions taken by the policy makers, the automotive industry, and other stakeholders impact the region’s future vehicle landscape.

Significant uncertainty remains around the European powertrain strategy and the future mix beyond 2035, against a backdrop of a progressively more challenging economic environment. In this context, the need for OEMs to meet customer expectations for affordability, usability and real‑world performance remains critical.

Lubricants clearly have an important role to play in the wider decarbonisation journey across the existing and future vehicle parc. Modern lubricant technologies already deliver fuel economy benefits, protect increasingly complex engine and aftertreatment hardware, and support durability and longevity.

As hybridisation grows, lubricant formulations must also address challenges arising from the different operating modes, including higher thermal loads and intermittent engine operation. This could present opportunities for lubricant makers to develop products specifically tailored to meet the requirements of these complex systems. Infineum has been testing hybrid-specific formulations over several years and is ready to support this growth market.

Click here to read more about the technical requirements of hybrid-specific lubricants.

Meeting the EU’s overall greenhouse gas objectives by focusing on new vehicle tailpipe regulations alone may not be sufficient. Again, lubricants have a role to play, particularly in enabling compatibility with alternative non‑fossil fuels. Here they can be used either as fuel extenders, such as biofuel blends, or as stand‑alone options, for example, e‑fuels or hydrogen‑based solutions. Continued lubricant innovation can support incremental efficiency gains and emissions reductions across ICE, hybrid and electrified powertrains alike.

Infineum is committed to powering a greener future and continues working to help ensure the success of the market transition towards net zero.

Sign up here to receive email alerts so that you never miss out on new Future of Mobility content from Infineum - and make sure you follow Infineum Additives on LinkedIn.

Sign up to receive monthly updates via email