Base stocks

The latest on base stock trends

30 September 2025

24 March 2026

ICIS assesses the current landscape and explores what the future may hold 30 years ahead

The ICIS World Base Oils and Lubricants Conference is seen as the place where industry’s most influential leaders meet, make decisions and shape the future – and the 30th anniversary event held in London fulfilled these expectations. Insight reports on the keynote session delivered by the host, global chemical and energy market analysts ICIS, which looked closely at current and near term global base oil market trends and explored potential scenarios well into the future.

The London ICIS World Base Oils and Lubricants Conference was a real celebration of the event’s 30th anniversary. A keynote presentation from ICIS jointly delivered by Michael Connolly, Head of Refining and Base Oils Analytics, Stefano Zehnder, Vice President of Consulting, and Amanda Hay, Global Base Oils Lead, supports this theme, with a deep dive into what’s influencing today’s landscape followed by some insights into how the market might look 30 years from now.

The session starts with a look at 2025-2026 signals including the main supply and demand drivers, price volatility linkages (such as geopolitics, freight and energy), and near-term expectations. Here, ICIS reports that global base oil markets are in flux, with new Asian capacity coming on stream, tightening Group I supply in Europe, and a trend for more Group III self-sufficiency in the United States (US).

“2025 and 2026 will shape the future demand for base oils and, what we expect to see is the markets settling into a period of oversupply.”

Amanda Hay, ICIS

While base oil capacity is expected to increase, ICIS suggests there will be an overall downward demand trend for the three key upstream products (Group I, II and III), with a general expectation that supply will outpace demand. Looking more closely at the different products, there has been some tightness in supply of Group I owing to refinery closures in Europe, but demand remains for these heavier grades. Group II is currently over supplied, relative to demand, while Group III is in a fairly tight supply/demand balance. These two higher quality products command a premium but, the demand for base oil quality varies significantly from region to region.

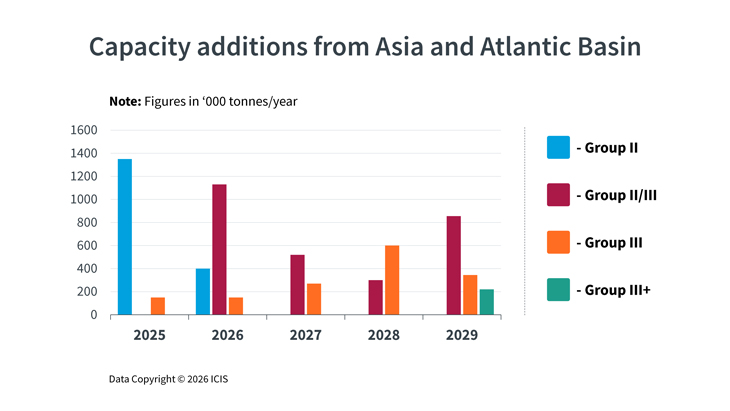

ICIS forecasts that the market will remain over-supplied in the next five years as capacity comes online from Asia and the Atlantic Basin regions. Predominantly this is likely to be the case for Group II, as refinery expansions and new projects are expected to come online before market demand picks up in the emerging markets.

However, not all projects are expected to target the same markets. In Asia, for example, ICIS says expansions at ExxonMobil in Singapore and Luberef in Saudi Arabia are focused on export markets, while the new capacity coming online in India and China is for local consumption. In the US, a wave of expansions and new projects are coming online to help satisfy the growing demand for Group III. A similar picture is emerging in Brazil, where production is shifting from Group I to Group II to meet evolving market needs. ICIS foresees that this localisation of production could lower the need for base oils imports into US and Brazil in the future.

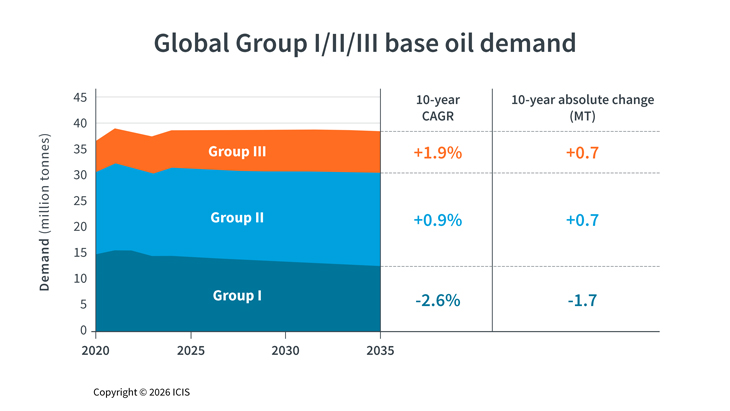

The ICIS session continues with a look at how new capacity in Asia and the Middle East, combined with evolving demand from the automotive and industrial sectors, is expected to reconfigure regional balances and the demand slate. Starting with a global overview out to 2035, ICIS reports relatively flat total demand but small growth for Group II and III and a continued decline in demand for Group I.

Today most of the demand across base oil groups comes from Asia and North America. However, demand patterns are changing, with some exciting growth markets emerging.

“It is increasingly important to think regionally in your business, matching products with the different regional requirements and spotting opportunities for growth.”

Stefano Zehnder, ICIS

ICIS sees significant growth in demand from the traditional markets of Africa, Asia and the Middle East. Africa is leading the regional growth as a percentage, but the fastest growing single market is India. Here, the evolving quality of engine and industrial oils is one aspect, but also volume drivers including population growth, an expanding car parc and higher GDP per capita can also be expected to influence the market. In Northeast Asia, North America and Europe there is a different picture. Here demand is flat or in decline – while there is still an evolution in quality as lubricants shift to even lower viscosities and marine moves to Group II, the volume drivers are absent in these regions.

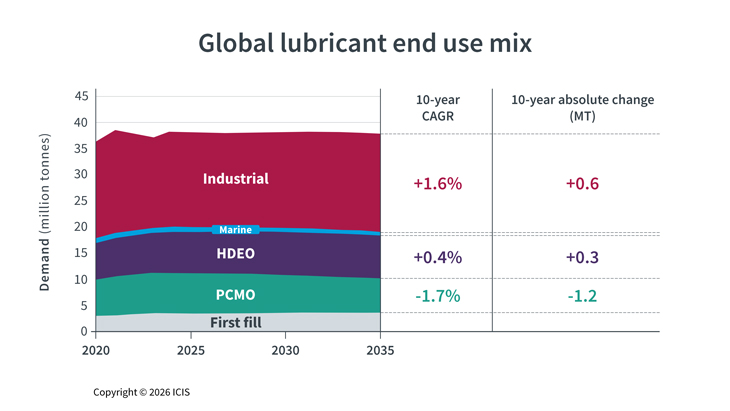

In terms of finished lubricant demand, again ICIS forecasts a relatively flat future, with a decline in passenger car engine oils and limited growth in heavy-duty engine oils and industrial oils.

Again it is a mixed regional picture with the mature markets in decline owing to the faster pace of vehicle electrification while growth is anticipated in Asia, Africa and Latin America markets.

Looking even further ahead, ICIS expects the evolving energy transition, increased scrutiny on circularity and sustainability, and policy pathways to shape future base oil requirements. The final section of their session starts with a look at all the trends that will continue to shape our industry for many years to come in terms of demand, trade and supply.

On the demand side, the mega-trends are the pace of vehicle electrification, changing lubricant standards and the industrialisation of emerging markets. The session moves on to take a closer look at the impact of trends in the passenger vehicle market. In terms of the challenges, ICIS sees a slowdown in the growth of the global passenger car fleet with only a 1.3% CAGR forecast from 2025-2050. By the end of this period they expect significant growth in the full battery electric vehicle (BEV) and hybrid electric vehicle market share in China, Europe, and North America - although lower growth elsewhere. While BEVs require less lubricant over their lifetime vs internal combustion engines (ICE), hybrids and ICE use similar volumes of fluids. This means the future mix of these technologies, which is very hard to predict, will heavily influence future base oil and finished lubricant demand.

Faster BEV growth and OEM demands for longer drain intervals could lower lubricant (and base oil) demand. However, ICIS also sees industrial growth in India, Southeast Asia and parts of Africa increasing lubricant demand from those regions and putting a greater focus on higher quality formulations.

“Emerging markets will be a key growth driver for demand, and the future mix of base oil groups will be reshaped by evolving standards.”

Michael Connolly, ICIS

In terms of future base oil trade, ICIS sees the shift in trade policies as a key driver for change and expects to see impacts to cross-border trades through both trade and geopolitical tensions along with the introduction of trade tariffs.

On the supply side, refinery closures and investments, supply chain disruptions and sustainability initiatives are all likely to influence the future.

ICIS says refinery closures are likely to further shorten Group I supply while continued strategic investments in new facilities and refinery expansions should make higher quality Group II and Group III products more widely available. However, at the same time, geopolitical tensions could increase supply chain disruption, which highlights the need to diversify supply chain and feedstock procurement strategies. On top of these trends, ICIS sees the increased focus on sustainability initiatives in response to policies and regulatory pressure as another driver for change. Here, the focus will be on finding the best ways to track and reduce carbon emissions and on improving product circularity.

“We expect to see a greater scrutiny on life cycle emissions and circularity and an increased focus on operational resilience amidst global uncertainty.”

Michael Connolly, ICIS

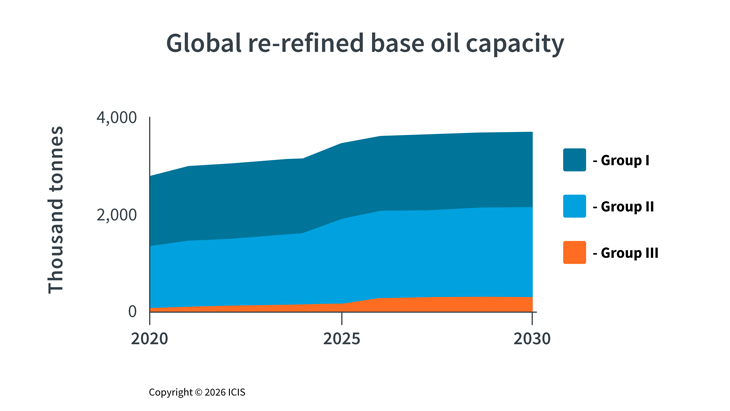

Taking a closer look at re-refined base oils (RRBO), ICIS tracks a 33% growth (~ 1 million tonnes) in global RRBO capacity between 2020 and 2030. While the majority remains at Group I/II quality, enhanced lubricant standards and controlled collection are now allowing a greater percentage of re-refined materials to be at Group III quality.

Regulations across the globe regarding RRBO still differ substantially, with some focussing on collection and extended producer responsibility, while others require a certain re-refined content in finished lubricants. And, as ICIS notes, many countries have no RRBO regulations in place at this time. However, ICIS thinks there is likely to be a growing interest in the circularity and carbon footprint reductions RRBO can offer.

In an uncertain world, it looks likely that sustainability, geopolitics, evolving regulations, increased volatility and structural change are all going to be important factors that shape the future base oil and lubricant markets. And, given the high level of uncertainty ahead, it will be increasingly important for businesses in this sector to keep up to date on the trends that are transforming the future.

Note - This presentation was delivered in February 2026, before the onset of conflict in Iran in March 2026. Unless long term sustainable damage is made to those base oils plants in the Persian Gulf or it creates a lasting issue slowing down global macroeconomics, the longer term trends are likely to still hold true, despite greater volatility in the near term.

Sign up here to receive free regular Infineum Insight updates direct to your inbox, and make sure you follow Infineum Additives on LinkedIn.

Sign up to receive monthly updates via email