Fuels

Driving hydrogen forward

21 January 2025

13 April 2021

Post-COVID demand recovery and supply tightness have far reaching industry implications

Saying 2020 was a tough year for the refining industry is something of an understatement. The anticipated gains from the IMO 2020 marine fuel sulphur regulation did not materialise and the COVID-19 pandemic has hit supply, demand and profits. As we begin to emerge from the turmoil, Dean Clark, Infineum Lubricity Venture Manager, explores how the potential recovery opportunities offered by renewable biodiesel production may be hindered by raw material availability.

As we entered 2020, many refiners were expecting to appreciate a significant windfall due to changes in the IMO 2020 global marine fuel specifications. The hope that margins would be higher than usual may have led refiners to feel optimistic about the short-term outlook. But then the COVID-19 pandemic struck and 2020 did not play out the way refiners – or anyone else – had expected.

Demand for fuels decreased as the pandemic spread and global oil demand fell off a cliff.

Excessive fuel stocks caused major disruption within supply chains and only compounded existing low margins. As the vaccine programme rolls out, the world is now on the edge of a tentative recovery. However, despite the first signs of optimism, refiners still face many constraints such as declining demand in jet fuel, which is not projected to reach pre-COVID levels to 2025 along with continued supply disruptions.

The refining sector is potentially seeing a round of significant restructuring. In an attempt to improve profitability, more refiners are entering the biofuels environment and here, renewable diesel hydrotreated vegetable oil (HVO) offers opportunities. Enhanced biofuels targets, most notably the new European Renewable Energy Directive (RED II), are creating a favourable context for investments in renewable diesel capacity. This in turn though puts refiners into the more traditional oleochemicals environment since the feedstocks for HVO are also very often used by this market.

Oleochemicals are used in a wide variety of applications,

Oleochemicals are used in a wide variety of applications,Oleochemicals derived from vegetable oils and animal oils & fats are used in anything from peanut butter to soaps or automotive tyres and fuel additives to name a few of their applications. Refiners, who generally have a clear line of sight from crude to the finished product, will have very little visibility of the oleochemicals supply chain. Going forward, with significant feedstocks needed for renewable diesel capacity, the elements impacting both supply and demand are going to be uncertain at best!

The availability of oleo feedstocks (e.g. rapeseed, palm, tallow, tall oil, soy) in the near to longer term is inundated with complexity.

Interdependency in many differing markets will significantly impact both supply and price. For example, we have seen shortages of tallow-derived oleic acids because of the increased use of raw tallow for biodiesel production in Europe. At the same time, political objections around the use of palm in biofuels have also driven the use of other feedstocks. Add in a massive increase on the need for soy in China to meet the needs of the agriculture sector together with poorer recent rapeseed harvests in Europe and it a picture of the complexity begins to emerge.

In many applications that use oleochemicals, it is not easy to switch to other feedstocks owing to either product approvals or exacting standards for the final application. In some cases, fuel additives can be used to help to meet the required standards. In a previous article ‘Are all lubricity products equal?’ I talked about the delicate balance between cost and sustainable lubricity performance and how robust and reliable overall performance is critical to maintaining refinery operations.

It is expected that, fatty acid consumption will rise in line with a growing population, as demand for cosmetics and personal care products grows, which are both big users of these feedstocks. The additional expansion in demand for fatty acids and related feedstocks for use in fuels is adding to market growth expectations. This in turn puts additional pressure on other oleic acids with a growing number of countries focusing on these second-generation biofuels instead of traditional crop-based fatty acid methyl esters (FAME) biofuels.

The COVID-19 impact on the production of oleo feedstocks ranges from limiting the movement of migrant workers in the farming industry, which impacts harvesting to claims that some nutritional supplements in rapeseed may help prevent or mitigate COVID-19 severity. If we add the disruption in the marine industry, where social distancing measures are impacting the workforce thus increasing the time and length of supply chains, this all adds up to a very uncertain short to medium term outlook for feedstock supply and price. And, the current supply/demand environment does not consider pent-up demand.

Currently, the pandemic means many industries using oleo feedstocks are running in a reduced capacity mode.

Demand in many areas including automotive manufacturing or restaurants and hospitality will begin to come back online as the vaccine roll out takes hold, increasing the need for oleo feedstocks and intensifying market tightness. Having agreed contracts in place for supply that are consistent with future needs is a must going forward. Reliability of supply could well be a necessary trade off against cost because securing the lowest price for something that is not available has no material benefit.

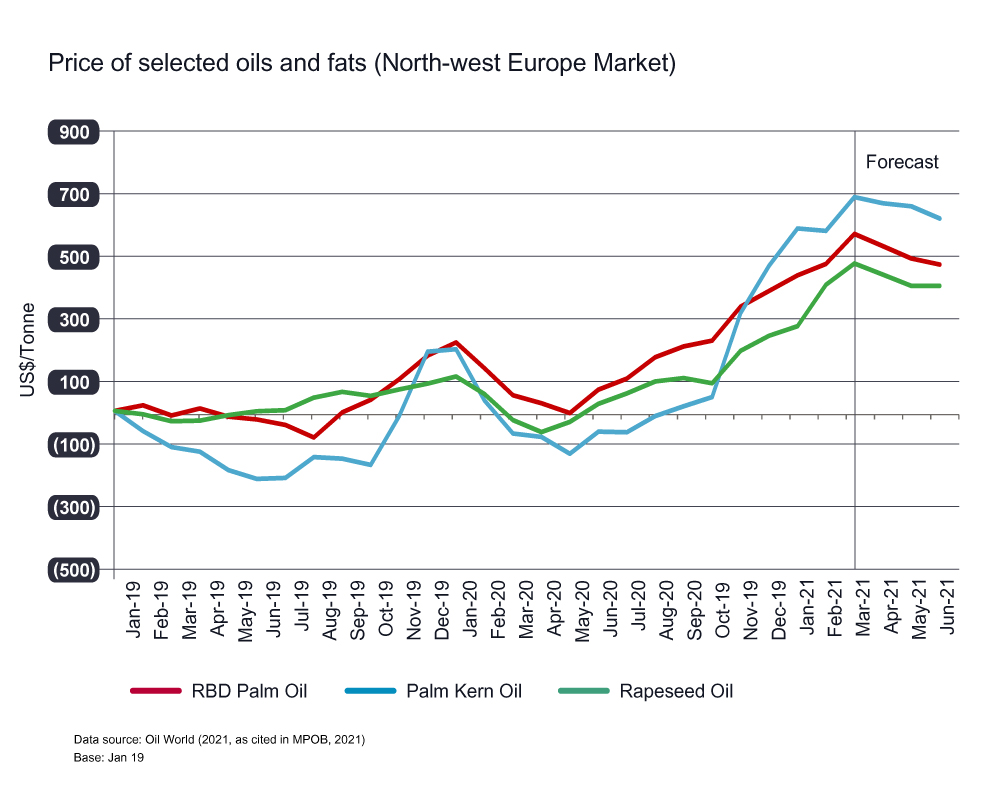

Oils and fats market in North-west Europe is at record pricing levels aligned to tight supply/demand environment

Oils and fats market in North-west Europe is at record pricing levels aligned to tight supply/demand environment

The consensus of opinion is that we have a very bumpy ride ahead of us. The supply/demand outlook for oleo feedstocks will be tight. Flexibility in raw material sources is likely to be the best form of risk mitigation.

The ability to easily switch from one feed material to another based on either price, technical fit or availability appears to offer the best way to ensure reliability.

This is not easily achieved in many sectors, but it may be the only option to manage the challenges ahead! Here, fuel additives can be used to ensure requirements and specifications continue to be met when switching between raw materials.

Sign up to receive monthly updates via email